Date

August 31, 2023

Exploring Open Finance: Opportunities and Challenges

Open finance is a broader term than open banking, which refers specifically to the sharing of financial data and services between banks and other financial institutions.

What does Open Finance really mean for financial markets and customers?

What is Open Finance?

Open finance is a broader term than open banking, which refers specifically to the sharing of financial data and services between banks and other financial institutions.

Open finance, on the other hand, applies to a wider range of financial services, including savings, investments, mortgages, and insurance. This means that open finance has the potential to affect a radically broader range of financial products and services, and potentially even a customer’s entire financial footprint.

Open finance will give consumers the ability to authorize third-party providers to access their financial data and initiate transactions on their behalf. This can provide consumers with more control over their financial data and allow them to take advantage of new and innovative financial products and services.

The European Union Commission has announced that it will present an open finance regulatory framework during 2022/2023, which may mandate open finance by law.

This framework is expected to require financial institutions to put in place and maintain secure and standardized APIs to share data with third-party providers at the customer’s request. This will help to ensure that open finance is implemented in a secure and transparent manner.

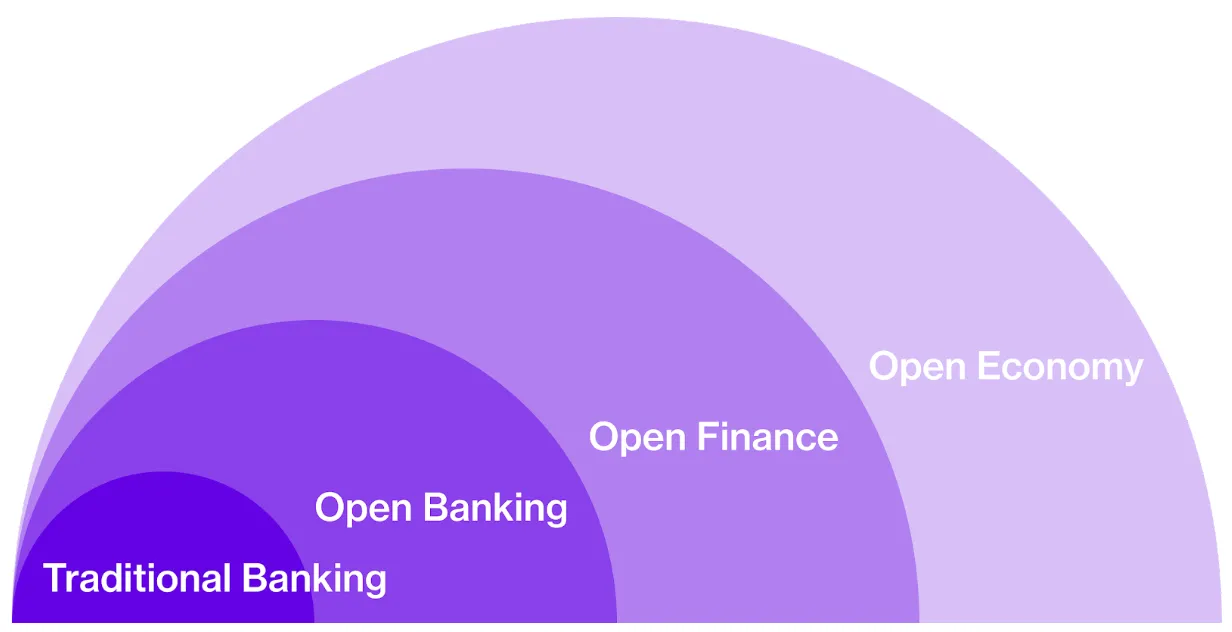

From traditional banking to the ‘Open Economy’

The evolution of the banking industry can be divided into four phases:

Closed or traditional banking, where financial institutions originate and distribute their own products, such as current accounts and payment services.

Open banking, which requires financial institutions to provide payment account information to third-party providers on customer request, enabling them to use and act on this information for account aggregation and payment processing.

Open finance is the third phase of this evolution, which will likely require financial institutions to provide access to all consumer financial data on customer request to third-party providers. This will enable third-party providers to use this information for a wide range of purposes, such as credit assessments or customized insurance premiums.

The final phase is the open economy, which is an extension of open finance and involves the integration of all consumer data on their request, providing this information to one or many third-party providers who can then use or act upon it. This will result in a more integrated financial services ecosystem for customers, which will continue to disrupt traditional business models and challenge financial institutions.

Implications for Financial Institutions

Open finance is a broader term than open banking, and it has the potential to affect a wider range of financial products and services. This means that Financial Institutions such as banks and Asset Managers and Insurance Companies will need to be prepared for the implementation of open finance in a similar way to open banking, but for a larger scope of products and services.

Open finance could disrupt traditional banking products such as savings, investments, pensions, mortgages, and insurance. This means that Financial Institutions will need to invest in and maintain real-time connectivity to data through APIs, in order to enable the sharing of data with third-party providers. This may involve some additional costs and efforts for Financial Institutions, but it will also provide them with the opportunity to improve their customer experience and offer new and innovative products and services.

However, open finance also has the potential to create challenges for Financial Institutions. For example, they may face increased competition from third-party providers who can offer more personalization to customers. This could put pressure on Financial Institutions’ margins on their core products, such as savings and investment accounts. Therefore, it is important for Financial Institutions to be prepared for the implementation of open finance and to find ways to adapt and compete in this changing financial landscape.

Implications for Customers

Open finance has the potential to enable a new way of providing financial services, known as “finance-as-a-lifestyle”. This means that financial services will be integrated into people’s daily lives and available to them whenever they need or want them, with personalized products and services that meet their individual needs and preferences.

Open finance will push financial institutions to transform and adapt to this new way of providing financial services. It will require them to prioritize the financial welfare of their customers as the primary objective at all times, and to tailor services to individual customer needs and preferences.

In order to achieve this, financial institutions will need to use technology and data to better understand their customers and provide them with the facilities that they need. This will involve leveraging the power of open finance and decentralized technologies, such as blockchain and distributed ledger technology, to create a more transparent, secure, and efficient financial system that is focused on delivering value to customers.

Implications for Businesses

Open finance has the potential to provide a range of benefits to small and medium-sized enterprises (SMEs). It can help them to achieve their core objectives of driving business growth, increasing effectiveness, and achieving employee wellness, as well as driving customer engagement.

Open finance can help SMEs to achieve these objectives by providing them with access to a wider range of financial products and services that are tailored to their individual needs and preferences. For example, open finance can enable SMEs to access data-driven credit assessments or customized insurance products that are designed to help them manage their risks and grow their businesses.

Additionally, open finance can help to automate many of the non-core tasks for which SMEs are responsible, such as bookkeeping and accounting. This can free up time and resources that SMEs can then use to focus on their core business activities and drive growth.

Overall, open finance has the potential to be a powerful tool for SMEs, providing them with the opportunity to succeed and grow in today’s competitive business environment.

Crosskey can help You

Crosskey has experience in building open banking APIs, and therefore is well-positioned to help you in building open finance APIs.

To help you as a bank or financial service provider build open finance APIs, Crosskey can provide expertise and guidance on the technical aspects of API development, such as design, implementation, and testing. Open Banking Market (crosskey.io).

Crosskey can also assist in understanding the regulatory requirements and industry standards that apply to open finance and help you to ensure that your APIs are compliant with these requirements. We are experts in security, simplicity, and ease of use with integrated compliance.

Our solutions at Crosskey cover everything from traditional banking to ebanking, card & mobile payment, capital markets and OpenBanking. Our customers include cutting edge fintech companies and multiple Nordic banks.

If you want to know more and how we can help you to drive growth and build even more success, please contact us for more discussions.